Workers’ compensation classification codes are the foundation of workers’ compensation insurance.

Class codes are where to begin and the most impactful factor of an employer’s/ insured’s premium for coverage.

What Are Worker’s Compensation Classification Codes?

Workers’ compensation class codes are numerical representations of specific work processes and job classifications assigned to an employer’s business.

There are over 700 unique codes with detailed descriptions used to differentiate between various job duties or “scope of work performed” by employees.

The source for most workers’ compensation classification codes in the U.S. is the National Council on Compensation Insurance (NCCI)—an independent organization that collects and analyzes statistical data for workers’ compensation rating.

Operations for NCCI are funded primarily by insurance companies who, in turn, utilize the resources and services provided.

NCCI establishes and maintains workers’ compensation class codes publishing them in the Scopes Manual, a vital resource for insurance professionals.

Why Is It Important To Have The Correct Workers’ Comp Class Code?

If employees are not classified correctly, claim frequencies and loss ratios may be out of kilter with what is expected for the class code(s) to which they are incorrectly assigned.

Likewise, the statistical information used by rating bureaus such as NCCI to track payroll, loss patterns, and loss ratios will be flawed and not 100% accurate for the incorrect class code and the correct class code, which should have been used for the employer.

What Is The Best Way For An Insured To Save Money On Workers’ Compensation Insurance?

Having a highly qualified agent is key.

However, final premiums are provided by insurance underwriters. A business that builds a long, trusting relationship with one carrier solidifies consistency and provides the most likely chance to save money in the long run.

Worker’s Compensation Classification Codes: A Case Study

Twenty-five years ago, Fancy McDay started making corsages and boutonnieres for local high school students attending special events like homecoming and prom.

Her flowers and artistic work were exceptional and within a year, Fancy asked her sister to help and opened a floral shop, Fancy’s Flowers.

Today, Fancy’s Flowers has expanded to four florist locations in the metro area selling plants, flowers, giftware and decorative home items.

Fancy’s Flowers also operates a separate 100-acre tract of land with greenhouses to grow fresh, native flowers, and two years ago purchased a large warehouse facility to store items for distribution to other florists in a three-state area.

Fancy even propagated a new variety of mum and obtained exclusive variety rights for the flower she calls Fancy’s Favorite.

Annie Agent stopped by Fancy’s largest floral store one afternoon to look for a plant to give to a client who had recently had a baby.

The store also served as corporate headquarters and Annie left feeling as if it were her lucky day.

Fancy overheard Annie mention to the salesclerk that she was an insurance agent.

Fancy’s agent had recently retired, and she was not comfortable with the new agent appointed to manage her account.

Fancy asked Annie if she would look at her insurance portfolio and provide quotes for her various coverages.

And if Annie could hurry, she would be able to write the workers’ compensation piece first because current coverage had been non-renewed and Fancy had not yet received an alternate quote.

Annie obtained a copy of Fancy’s current workers’ compensation policy, NCCI Experience Rating Worksheet, and a signed authorization to order loss runs from the current carrier.

Relying solely on the expiring workers’ compensation policy without interviewing Fancy or having researched any information about her company, Annie completed a workers’ compensation insurance application and submitted it to various carriers, including one that had a great program for florists.

She advised loss runs were ordered and would be forwarded upon receipt.

Annie copied verbatim the information on Fancy’s expiring workers’ compensation and included the following on the application:

| Class Code | Description | Remuneration (Payroll) |

| 8017 | Store-Retail NOC | 2,300,000 |

| 7380 | Drivers | 350,000 |

| Experience Mod. Factor: 1.59 |

Three of the carriers to whom Annie submitted applications, including the one specializing in florists, declined within 24 hours due to the mod factor.

A fourth underwriter, Uma, acknowledged receipt of the application and mod worksheet and searched the internet for more information about Fancy’s Florist.

Uma found an article online spotlighting Fancy’s Favorite mum published in a flower journal.

And the Fancy’s Florist website had photographs of the insides of the stores showcasing flower arrangements and home décor.

Other information under the “services provided” tab of Fancy’s website included the wholesale distribution of floral supplies, and flower growing operations.

Included were pictures of fields with rows and rows of flowers in bloom, and the greenhouses filled with plants.

And outside the warehouse located in another town 12 relatively new box trucks with professional graphics on each of colorful pots and giftware and the words “Fancy’s Florist…Your favorite source for all your floral needs,” were pictured.

As a result, Uma understood why the mod factor might be so high and the current carrier non-renewing—the class codes did not adequately represent the exposure according to information obtained.

Uma asked Annie for the following information:

- Currently valued loss runs with explanations of any individual losses over $25,000

- A complete description of operations

- Addresses of all locations

- Payroll specific to the retail florist locations (stores) only

- Details about the greenhouses and growing business including associated payroll

- Specifics on the warehouse and distribution services and applicable payroll

- Information on the trucks and drivers and their payroll

Annie Agent provided the additional information to Uma who completed her analysis and provided a quote with the following class codes:

| Class Code | Description | Remuneration (Payroll) |

| 0035 | Farm: Florist & Driver | 1,000,000 |

| 7380 | Drivers NOC | 350,000 |

| 8017 | Store-Retail NOC | 300,000 |

| 8018 | Store-Wholesale NOC | 1,000,000 |

Using the appropriate class codes increased the premium by about $50,000 over the price using only the florist and driver classifications, which was enough premium to make sense to Uma to quote the account.

Annie Agent, with great counsel from Uma the underwriter, explained to Fancy that the high experience rating factor and non-renewal of the current policy were most likely a result of improper classification.

Annie added that getting the class codes corrected now might save Fancy money in the long run; rates would be charged according to actual work done.

In the meantime, Fancy’s previous agent was only able to get an Assigned Risk quote—still with the incorrect class codes, but at a higher premium than Annie’s voluntary market quote with proper class codes.

Fancy bound Uma’s quote and appreciating the help, moved all insurance policies for Fancy’s Florist to Annie.

Four years later, Fancy’s rates are slightly lower.

However, her experience mod has come down dramatically so that her total premium is almost half what it was before Uma the extraordinary underwriter dissected the risk, corrected the class codes, and helped Annie obtain a loyal customer.

Uma is now Annie’s go-to underwriter for all her workers’ compensation questions and accounts.

Sometimes she cannot quote accounts Annie submits, but Uma always provides Annie with great advice.

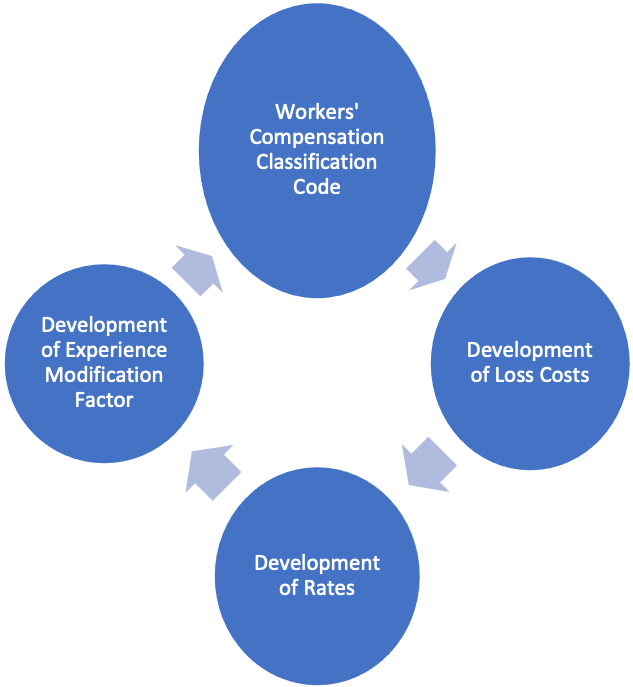

The Lifecycle Of A Workers’ Compensation Classification Code

Workers’ Compensation Classification Code

Currently a four-digit code assignment used to identify job duties/functions of specific categories of work.

EXAMPLE

Class Code 9082 RESTAURANT NOC

Applies to “traditional” restaurants providing wait service.

Development of Loss Cost

Statistical data is analyzed for each workers’ compensation classification code in each state to determine how much premium is needed per $100 payroll to cover expected losses.

EXAMPLE

Class Code 9082 RESTAURANT NOC

Loss statistics reveal it takes $1.11 per $100 payroll to cover expected losses of restaurant workers.

Development of Rates

A function of the loss cost (funds needed to cover expected losses) times a factor (multiplier) representing expected expenses, including commissions in each state.

EXAMPLE

Workers’ Best Insurance Company maintains a corporate office building, pays employees to underwrite, issue policies, bill policies and adjust claims, and pays 10% commission to agents who write policies with them.

Their statistics (maintained and analyzed by company actuaries) support it takes about $0.40 (forty cents) per $100 payroll to cover these expenses.

They develop a multiplier of 1.40 to apply to loss costs.

Class Code 9082 RESTAURANT NOC rate for Workers’ Best is $1.56 per $100 of payroll–$1.11 Rate X 1.40 Loss Cost multiplier.

Development of Experience Modification Factor

Designed to provide lower or higher rates to individual businesses (insureds) based on their loss experience as compared to other employers in the same/similar business within a state.

- A “unified” factor of 1.00 is given to new businesses and/or those with loss experience exactly average to others like it.

- A “credit” factor (anything below 1.00) means the business’s loss experience is better than the average than for others like it.

- A “debit” factor (anything higher than 1.00) means loss experience is worse than average.

Businesses and insurance agents use several terms when referring to an experience modification factor including:

- Experience modification rate

- Mod

- Mod factor

- X-mod

- E-mod

- EMR number

- NCCI factor

EXAMPLE

Rita’s Restaurant has had two workers’ compensation losses in the last three years totaling $728.00.

Rita’s experience is better than the average for other restaurants in her state so NCCI develops an Experience Modification Factor of 0.87 for Rita’s.

Rita’s is insured with Workers’ Best and is charged a “net” premium rate of $1.36 per $100 payroll.

Class Code 9082 RESTAURANT NOC rate of $1.56 X 0.87 Experience Modification Factor = $1.36.

Understanding proper workers’ compensation classification and how it helps control costs allows business owners to get the best accurate pricing and boost the bottom line.

If you have questions about correct classification during the underwriting, pricing, policy issuance, or audit process or anytime while a policy is in effect, contact an AIA professional. We’re ready and willing to help you find the answers you need.